Compensation costs for civilian workers increased 0.5 percent, seasonally adjusted, in the 3-month period ending in September 2020. Wages and salaries increased 0.4 percent and benefit costs increased 0.6 percent.

Personal income increased $170.3 billion (0.9 percent) in September. Disposable personal income (DPI) increased $150.3 billion (0.9 percent) and personal consumption expenditures (PCE) increased $201.4 billion (1.4 percent).

The September Prices Received Index 2011 Base (Agricultural Production), at 89.0, increased 0.9 percent from August and 1.1 percent from September 2019. The Crop Production Index was up 1.3 percent from last month and 5.9 percent from September 2019. The Livestock Production Index increased 0.2 percent from August, but decreased 3.7 percent from September 2019.

Farmers received higher prices during September for lettuce, hogs, corn, and soybeans but lower prices for milk, broilers, potatoes, and hay. In addition to prices, the indexes are influenced by the volume change of commodities producers market; in September, there was increased monthly volume for soybeans, corn, apples, and dry beans and decreased sales of cattle, wheat, cotton, and strawberries.

Friday, October 30, 2020

Thursday, October 29, 2020

After bounce economy still producing less

Real gross domestic product (GDP) increased at an annual rate of 33.1 percent in the third quarter of 2020, according to the advance estimate released by the Bureau of Economic Analysis. In the second quarter, real GDP decreased 31.4 percent.

To put this in perspective, at the end of 2019, the US had a $19.25 trillion economy. After the third-quarter rebound, the US had an $18.58 trillion economy.

To put this in perspective, at the end of 2019, the US had a $19.25 trillion economy. After the third-quarter rebound, the US had an $18.58 trillion economy.

Tuesday, October 27, 2020

Durable goods manufacturing stabilizing?

New orders for manufactured durable goods in September increased 1.9 percent to $237.1 billion, the U.S. Census Bureau announced today. This increase followed a 0.4 percent August increase and was the fifth uptick in a row. Although the May, June, and July increases were substantially higher than in the past 2 months, the massive declines in March and April mean the year-to-date level of durable good orders are fully 10 percent below the same 9 months of 2019. Perhaps durable good orders are now in a "New Normal" pattern that is lower than the "normal" normal?

Monday, October 26, 2020

New home sales rebound pauses for breath

Sales of new single-family houses in September 2020 were at a seasonally adjusted annual rate of 959,000,

according to estimates released jointly today by the U.S. Census Bureau and the Department of Housing and Urban

Development. This is not much changed from the revised August rate of 994,000, but is 32.1 percent

above the September 2019 estimate of 726,000.

There were 284,000 new homes for sale at the end of September, about a 3.6 month supply at the current rate of sales.

There were 284,000 new homes for sale at the end of September, about a 3.6 month supply at the current rate of sales.

Saturday, October 24, 2020

Cattle on feed at record level for October

Cattle and calves on feed for the slaughter market in the United States for feedlots with capacity of 1,000 or more head

totaled 11.7 million head on October 1, 2020. The inventory was 4 percent above October 1, 2019. This is the highest

October 1 inventory since the series began in 1996.

Thursday, October 22, 2020

Housing starts back to pre-pandemic patterns

Privately-owned housing starts in September were at a seasonally adjusted annual rate of 1,415,000. This is 1.9

percent above the revised August estimate of 1,388,000 and is 11.1 percent above September 2019. Over the past 5 months, housing starts have climbed out of the crater they were dropped into from January through April.

Wednesday, October 21, 2020

Playing a little catch up

The combined value of distributive trade sales and manufacturers’ shipments for August, adjusted for seasonal

variation, was estimated at $1,452.4 billion, up 0.6 percent from July 2020, but down 0.4 percent from August 2019.

Manufacturers’ and trade inventories for August, adjusted for seasonal variations,were estimated at an end-of-month level of $1,919.2 billion, up 0.3 percent from July 2020, but down 5.5 percent from August 2019.

The total business inventories/sales ratio based on seasonally adjusted data was 1.32 at the end of August. The August 2019 ratio was 1.39.

U.S. retail and food services sales for September 2020 were $549.3 billion, an increase of 1.9 percent from the previous month and up 5.4 percent over September 2019

Industrial production fell 0.6 percent in September, its first decline after four consecutive months of gains. The index increased at an annual rate of 39.8 percent for the third quarter as a whole. Although production has recovered more than half of its February to April decline, the September reading was still 7.1 percent below its pre-pandemic February level.

Manufacturers’ and trade inventories for August, adjusted for seasonal variations,were estimated at an end-of-month level of $1,919.2 billion, up 0.3 percent from July 2020, but down 5.5 percent from August 2019.

The total business inventories/sales ratio based on seasonally adjusted data was 1.32 at the end of August. The August 2019 ratio was 1.39.

U.S. retail and food services sales for September 2020 were $549.3 billion, an increase of 1.9 percent from the previous month and up 5.4 percent over September 2019

Industrial production fell 0.6 percent in September, its first decline after four consecutive months of gains. The index increased at an annual rate of 39.8 percent for the third quarter as a whole. Although production has recovered more than half of its February to April decline, the September reading was still 7.1 percent below its pre-pandemic February level.

Thursday, October 15, 2020

Import and export prices

U.S. import prices rose 0.3 percent in September following a 1.0-percent increase in August. Prices for U.S. exports advanced 0.6 percent in September, after rising 0.5 percent the previous month. Over the past year, import prices declined 1.1 percent and export prices fell 1.8 percent.

The U.S. terms of trade with China edged down 0.1 percent in September, the first monthly decline since the index fell 2.6 percent in April. In contrast, the index for U.S. terms of trade with China rose 0.4 percent over the past year. Terms of trade indexes measure the relative price of exports in terms of import prices. The index for China is calculated as the all-exports-to-China goods price index divided by the corresponding all-import goods price index on a scale of 100.

The U.S. terms of trade with China edged down 0.1 percent in September, the first monthly decline since the index fell 2.6 percent in April. In contrast, the index for U.S. terms of trade with China rose 0.4 percent over the past year. Terms of trade indexes measure the relative price of exports in terms of import prices. The index for China is calculated as the all-exports-to-China goods price index divided by the corresponding all-import goods price index on a scale of 100.

Wednesday, October 14, 2020

CPI, PPI, and real weekly earnings creep up in September

The Consumer Price Index for All Urban Consumers (CPI-U) increased 0.2 percent in September on a seasonally adjusted basis after rising 0.4 percent in August and 0.6 percent in July.

The Producer Price Index for final demand advanced 0.4 percent in September, seasonally adjusted. Final demand prices rose 0.3 percent in August and 0.6 percent in July. Within the intermediate demand category, prices for processed goods rose 1.0 percent and the index for unprocessed goods increased 3.9 percent.

Real average weekly earnings increased 0.2 percent in September as a 0.1 percent decline in real average hourly earnings combined with a 0.3-percent increase in the average workweek.

The Producer Price Index for final demand advanced 0.4 percent in September, seasonally adjusted. Final demand prices rose 0.3 percent in August and 0.6 percent in July. Within the intermediate demand category, prices for processed goods rose 1.0 percent and the index for unprocessed goods increased 3.9 percent.

Real average weekly earnings increased 0.2 percent in September as a 0.1 percent decline in real average hourly earnings combined with a 0.3-percent increase in the average workweek.

Friday, October 9, 2020

Wholesale inventories back in line with sales

Inventories/Sales Ratio: The August inventories/sales (I/S) ratio for merchant wholesalers, except manufacturers’ sales branches and

offices, based on seasonally adjusted data, was 1.31. The August 2019 ratio was 1.35.

In April and May, the wholesale I/S ratios were 1.63 and 1.53, respectively. These values were substantially higher than any others posted in the past 10 years, and thus this indicator has returned to a more normal reading. Unfortunately, the sales base of the ratio, at $486.6 billion, is still 3-1/2 percent below its pre-pandemic level.

In April and May, the wholesale I/S ratios were 1.63 and 1.53, respectively. These values were substantially higher than any others posted in the past 10 years, and thus this indicator has returned to a more normal reading. Unfortunately, the sales base of the ratio, at $486.6 billion, is still 3-1/2 percent below its pre-pandemic level.

Wednesday, October 7, 2020

Revolving credit outstanding declines

In August, consumer credit decreased at a seasonally adjusted annual rate of 2 percent. Revolving credit decreased at an annual rate of 11-1/4 percent, while nonrevolving credit increased at an annual rate of 3/4 percent.

There is 3.3 as much outstanding nonrevolving credit, which includes motor vehicle loans and all other loans not included in revolving credit, such as loans for mobile homes, education, boats, trailers, or vacations, as outstanding revolving credit including "what's in your wallet."

There is 3.3 as much outstanding nonrevolving credit, which includes motor vehicle loans and all other loans not included in revolving credit, such as loans for mobile homes, education, boats, trailers, or vacations, as outstanding revolving credit including "what's in your wallet."

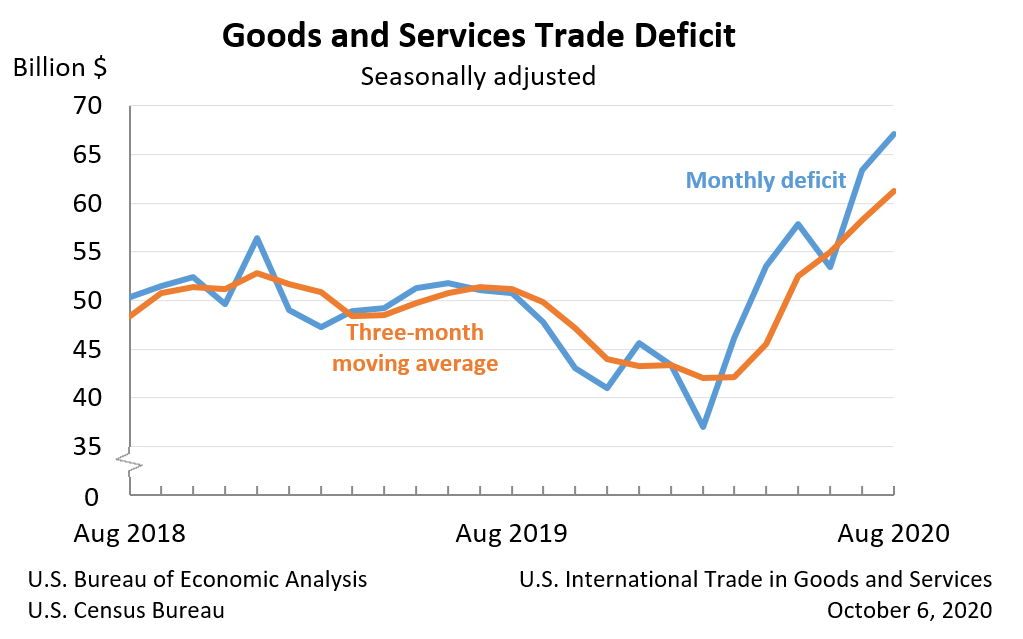

Tuesday, October 6, 2020

Trade deficit widens in August

The U.S. Census Bureau and the U.S. Bureau of Economic Analysis announced today that the goods and services deficit was $67.1 billion in August, up $3.7 billion from $63.4 billion in July (as revised). The two agencies cannot say how much of this might be related to the pandemic because such impacts "are generally embedded in source data and cannot be separately identified." That they almost certainly exist is seen at https://www.bea.gov/system/files/inline-images/trad0820.png

{kind=link}

Monday, October 5, 2020

I'm back

I'm starting this blog over in a more restrained format. I'll be making short remarks based on the official reports on the Principal Federal Economic Indicators (PFEI). On Friday, the U.S. Bureauof Labor Statistics (BLS) released the Employment Situation for September.

At the top side, the unemployment rate "declined to 7.9 percent" and nonfarm payrolls declined by 661,000.

The most remarkable thing about the report was its this-is-just-another-data-point tone. A move of half a percentage point in the unemployment rate is Hope-diamond rare; there have been only five other such movements in the past two decades. In 2020, a half-point decline is treated in the press as a "slowdown" in what might well be what the Wall Street people call a dead-cat bounce after the 11.2 full percentage point increase between February and April.

None of these developments should be considered in the same light as more ordinary economic fluctuations. Their origin is in the public health policy in response to the CoVID-19 pandemic. The good news is that this will result in shorter posts in this blog. The bad news will appear tomorrow in A Slight Right.

The most remarkable thing about the report was its this-is-just-another-data-point tone. A move of half a percentage point in the unemployment rate is Hope-diamond rare; there have been only five other such movements in the past two decades. In 2020, a half-point decline is treated in the press as a "slowdown" in what might well be what the Wall Street people call a dead-cat bounce after the 11.2 full percentage point increase between February and April.

None of these developments should be considered in the same light as more ordinary economic fluctuations. Their origin is in the public health policy in response to the CoVID-19 pandemic. The good news is that this will result in shorter posts in this blog. The bad news will appear tomorrow in A Slight Right.

Subscribe to:

Comments (Atom)